Paper Trading with Interactive Brokers¶

In this tutorial, you will learn:

What is paper trading

How to start paper trading with Interactive Brokers

Intro to paper trading¶

Definition

A paper trade is a simulated trade that allows an investor to practice

buying and selling without risking real money.

In this module, we will first set up a connection to Interactive Brokers Trader

Workstation (IB TWS).

Then, we will learn how to create basic contracts, request market data, manage

orders, and request account summary.

Setup Interactive Brokers API¶

Before setting up a connection to IB TWS, there are few tasks to be completed:

Visit InteractiveBrokers website, and open an account

Download IB API software from InteractiveBrokers GitHub account

Download TWS software from InteractiveBrokers TWS

Choose an IDE that you code in

Subscribe to market data

For detailed instructions, please refer to InteractiveBrokers Initial Setup.

Connect to Interactive Brokers TWS¶

Once finish the setup, it’s time to connect to IB TWS. Use

app.connect()

to establish an API connection.class App(EWrapper, EClient):

def __init__(self):

EClient.__init__(self, self)

# Establish API connection

# app.connect(ipAddress, portNumber, clientId)

app = App()

app.connect('127.0.0.1', 7497, 0)

app.run()

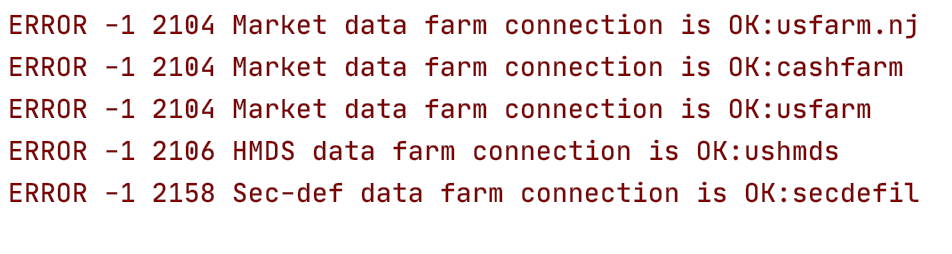

If you are successfully connected to IB TWS, you will get the below output in your

terminal.

Create Basic Contracts¶

Then, let’s create basic contract objects (trading instruments) such as stocks,

or fx pairs.

from ibapi.contract import Contract

# Create contracts - stocks

tsla_contract = Contract()

tsla_contract.symbol = "TSLA"

tsla_contract.secType = "STK"

tsla_contract.exchange = "ISLAND"

tsla_contract.currency = "USD"

# Create contracts - fx pairs

eurgbp_contract = Contract()

eurgbp_contract.symbol = "EUR"

eurgbp_contract.secType = "CASH"

eurgbp_contract.currency = "GBP"

eurgbp_contract.exchange = "IDEALPRO"

Request Market Data¶

Using the contract objects, we can request both streaming and historical market data.

Request Streaming Market Data¶

Use

app.reqMktData() to request streaming market data.class App(EWrapper, EClient):

# Receive market data

def tickPrice(self, tickerId, field, price, attribs):

print("Tick Price. Ticker Id:", tickerId, ", TickType: ", TickTypeEnum.to_str(field),

", Price: ", price, ", CanAutoExecute: ", attribs.canAutoExecute,

", PastLimit: ", attribs.pastLimit, ", PreOpen: ", attribs.preOpen)

# Request market data

# app.reqMktData(tickerId, contract, genericTickList, snapshot, regulatorySnaphsot, mktDataOptions)

app.reqMktData(1, tsla_contract, '', False, False, None)

Note that if you haven’t subscribed the market data, you will receive 10-15 minute

delayed streaming data. Before getting the delayed streaming data, make sure you use

app.reqMarketDataType(3) to switch market data type to delayed data.# Switch market data type

# 3 for delayed data

app.reqMarketDataType(3)

Request Historical Market Data¶

Use

app.reqHistoricalData() to request historical bar data.class App(EWrapper, EClient):

# Receive historical bar data

def historicalData(self, reqId, bar):

print("HistoricalData. ReqId:", reqId, "BarData.", bar)

# Request historical bar data

# app.reqHistoricalData(tickerId, contract, endDateTime, durationString, barSizeSetting, whatToShow, useRTH, formatDate, keepUpToDate)

app.reqHistoricalData(1, eurgbp_contract, '', '1 M', '1 day', 'ASK', 1, 1, False, None)

Manage Orders¶

Now, let’s try to make an order!

First, write some methods in EWrapper that are required for receiving all relevant

information on order opening, order status, and order execution.

class App(EWrapper, EClient):

def nextValidId(self, orderId: int):

super().nextValidId(orderId)

self.nextorderId = orderId

print('The next valid order id is: ', self.nextorderId)

def orderStatus(self, orderId, status, filled, remaining, avgFillPrice, permId, parentId,

lastFillPrice, clientId, whyHeld, mktCapPrice):

print("OrderStatus. Id: ", orderId, ", Status: ", status, ", Filled: ", filled,

", Remaining: ", remaining, ", AvgFillPrice: ", avgFillPrice,

", PermId: ", permId, ", ParentId: ", parentId, ", LastFillPrice: ", lastFillPrice,

", ClientId: ", clientId, ", WhyHeld: ", whyHeld, ", MktCapPrice: ", mktCapPrice)

def openOrder(self, orderId, contract, order, orderState):

print("OpenOrder. PermID: ", order.permId, ", ClientId: ", order.clientId,

", OrderId: ", orderId, ", Account: ", order.account, ", Symbol: ", contract.symbol,

", SecType: ", contract.secType, " , Exchange: ", contract.exchange,

", Action: ", order.action, ", OrderType: ", order.orderType,

", TotalQty: ", order.totalQuantity, ", CashQty: ", order.cashQty,

", LmtPrice: ", order.lmtPrice, ", AuxPrice: ", order.auxPrice,

", Status: ", orderState.status)

def execDetails(self, reqId, contract, execution):

print("ExecDetails. ", reqId, " - ", contract.symbol, ", ", contract.secType,

", ", contract.currency, " - ", execution.execId, ", ", execution.orderId,

", ", execution.shares , ", ", execution.lastLiquidity)

Place Orders¶

To place an order, use

app.placeOrder() to submit an order.# Place order

# app.placeOrder(orderId, contract, order)

app.placeOrder(app.nextorderId, eurgbp_contract, order)

Modify Orders¶

To modify the order, call

app.placeOrder() again with the order id to be

modified and the updated parameters.# Modify order

order_id = 1

order.lmtPrice = '0.82'

app.placeOrder(order_id, eurgbp_contract, order)

Cancel Orders¶

To cancel an order by its order id, use

app.cancelOrder().To cancel all open orders, use

app.reqGlobalCancel().# Cancel order by order Id

app.cancelOrder(app.nextorderId)

# Cancel all open orders

app.reqGlobalCancel()

Request Account Summary¶

Lastly, use

app.reqAccountSummary() to get the summarized account information.class App(EWrapper, EClient):

# Receive account summary

def accountSummary(self, reqId:int, account:str, tag:str, value:str, currency:str):

print("Acct Summary. ReqId:" , reqId , "Acct:", account, "Tag: ", tag, "Value:", value,

"Currency:", currency)

# Request account summary in base currency

app.reqAccountSummary(9002, "All", "$LEDGER");

# Request account summary in HKD

app.reqAccountSummary(9002, "All", "$LEDGER:HKD");

References

Attention

All investments entail inherent risk. This repository seeks to solely educate

people on methodologies to build and evaluate algorithmic trading strategies.

All final investment decisions are yours and as a result you could make or lose money.