Property price prediction¶

In this tutorial, you will learn:

The basics in macroeconomic analysis

The ways of analyzing macroeconomic indicators

The ways of analyzing real estate market data

How to build a property price prediction model

Intro to macroeconomic analysis¶

Macroeconomic indicators in Hong Kong¶

import random

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

import pandas as pd

import numpy as np

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import LabelEncoder

df.info() to print information of all columns.

The column information of macroeconomic data.¶

Univariate analysis¶

pandas.Dataframe.describe() to examine the

distribution of the numerical features. It returns the statistical summary such as mean,

standard deviation, min, and max of a data frame.seaborn.distplot()

to visualise the results with histograms.# Statistical summary

print(df[feature_name].describe())

# Histogram

plt.figure(figsize=(8,4))

sns.distplot(df[feature_name], axlabel=feature_name);

Bivariate analysis¶

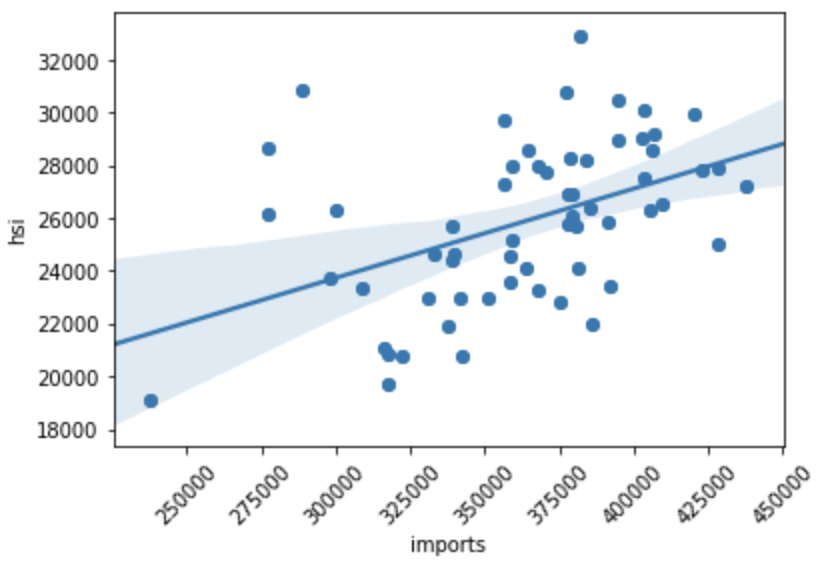

matplotlib.pyplot.scatter() and seaborn.regplot() to

visualize the relationship between two features.x = df[feature_name]

y = df['hsi']

plt.scatter(x, y)

plt.xticks(rotation=45)

fig = sns.regplot(x=feature_name, y="hsi", data=df)

An example of a scatter plot with a regression line.¶

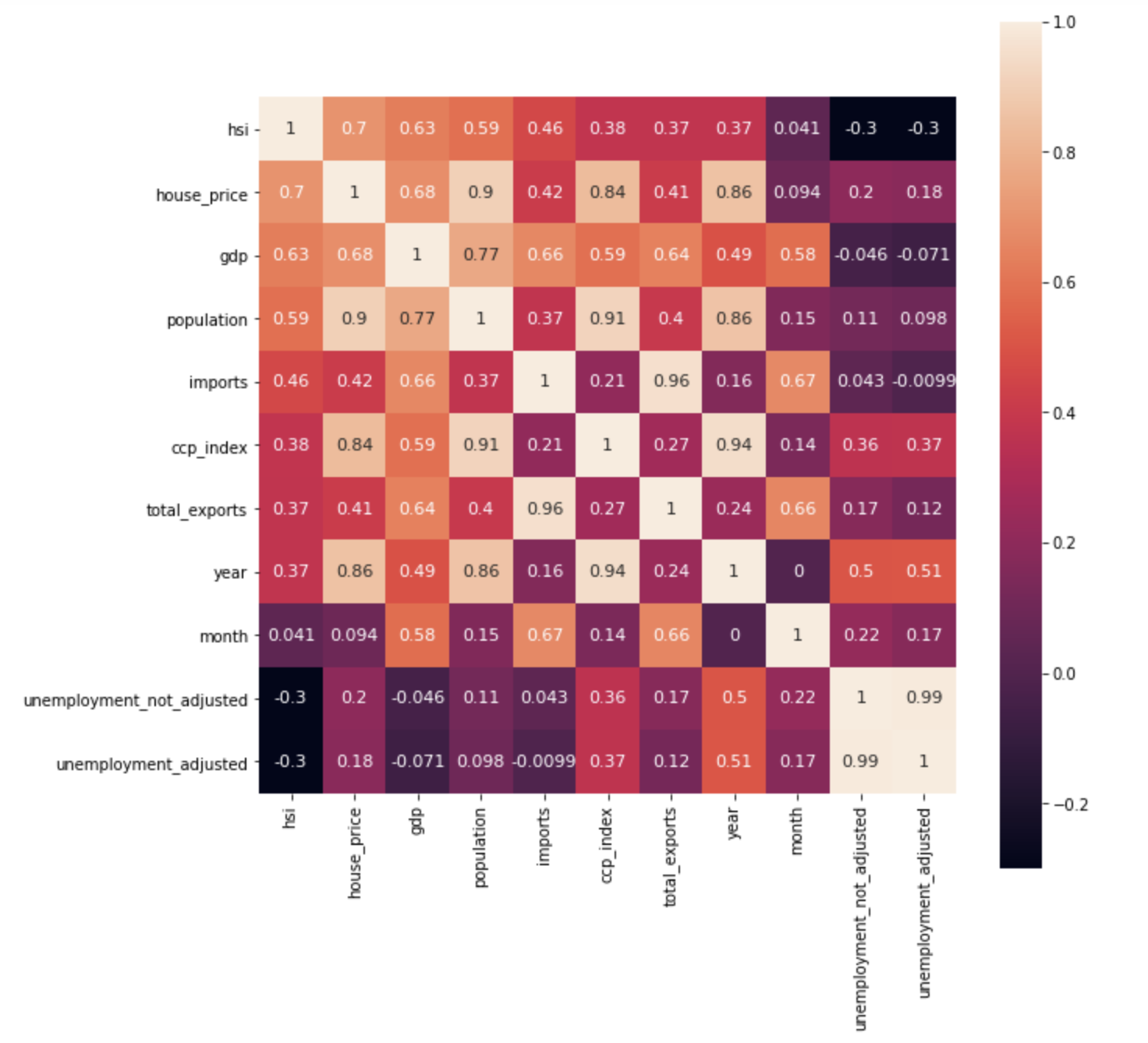

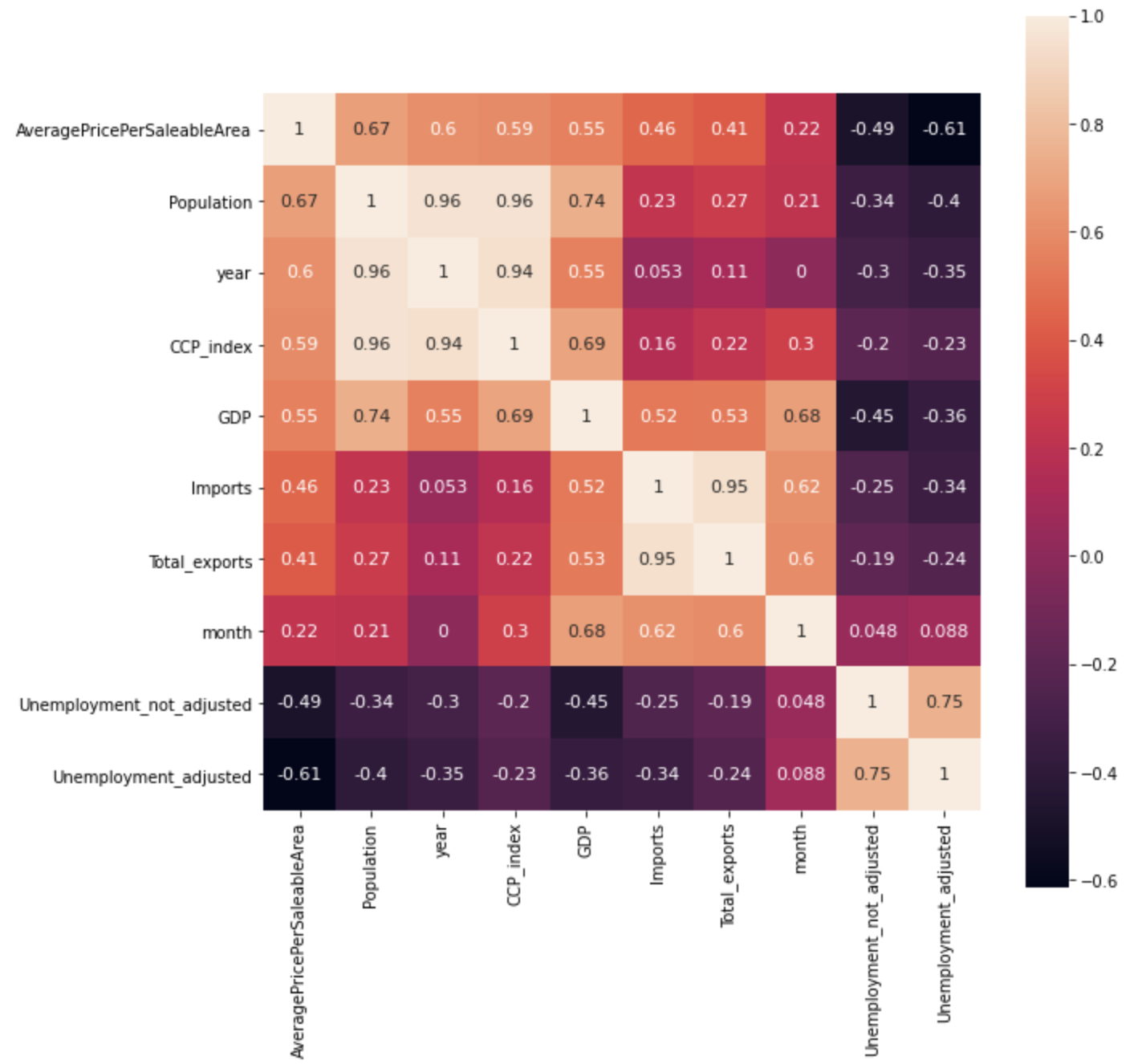

pandas.Dataframe.corr() and seaborn.heatmap() to compute

a pairwise correlation of features and visualize the correlation matrix.fig, ax = plt.subplots(figsize=(10,10))

cols = df.corr().sort_values('hsi', ascending=False).index

cm = np.corrcoef(df[cols].values.T)

hm = sns.heatmap(cm, annot=True, square=True, annot_kws={'size':11}, yticklabels=cols.values, xticklabels=cols.values)

plt.show()

Heatmap - macroeconomic indicators of Hong Kong.¶

The Hong Kong real estate market¶

Data pre-processing¶

1. Derive some useful features from existing features.

# Add new features

df['month'] = pd.to_datetime(df['RegDate']).dt.month

df['year'] = pd.to_datetime(df['RegDate']).dt.year

2. Drop unmeaningful features and features with too many missing values

# Drop unnecessary columns

df = df.drop([feature_name], axis=1)

3. Handle missing values by replacing NAN with a mean value of a feature

# Handling missinig values

# Fill with mean

feature_name_mean = df[feature_name].mean()

df[feature_name] = df[feature_name].fillna(feature_name_mean)

Label encode categorical features

le = LabelEncoder()

le.fit(list(processed_df[feature_name].values))

processed_df[feature_name] = le.transform(list(processed_df[feature_name].values))

Economic indicator analysis¶

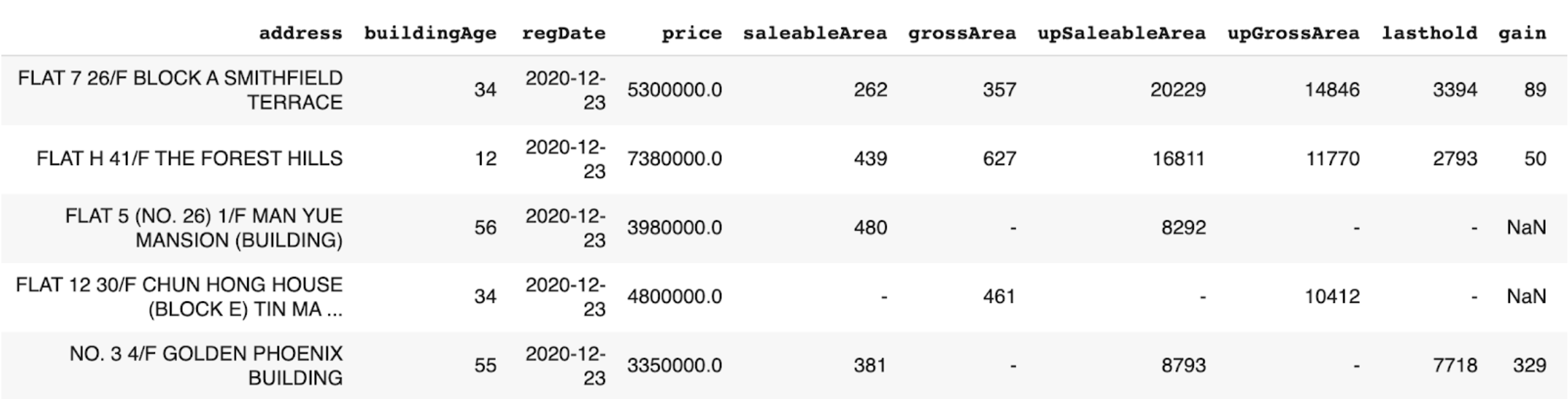

The data structure of transaction record (Centaline Property).¶

# calculate the monthly average house price

df = df.groupby(['year','month'],as_index=False).mean()

df = df.rename(columns={'UnitPricePerSaleableArea': 'AveragePricePerSaleableArea'})

Heatmap - economic indicators analysis.¶

Transaction record analysis¶

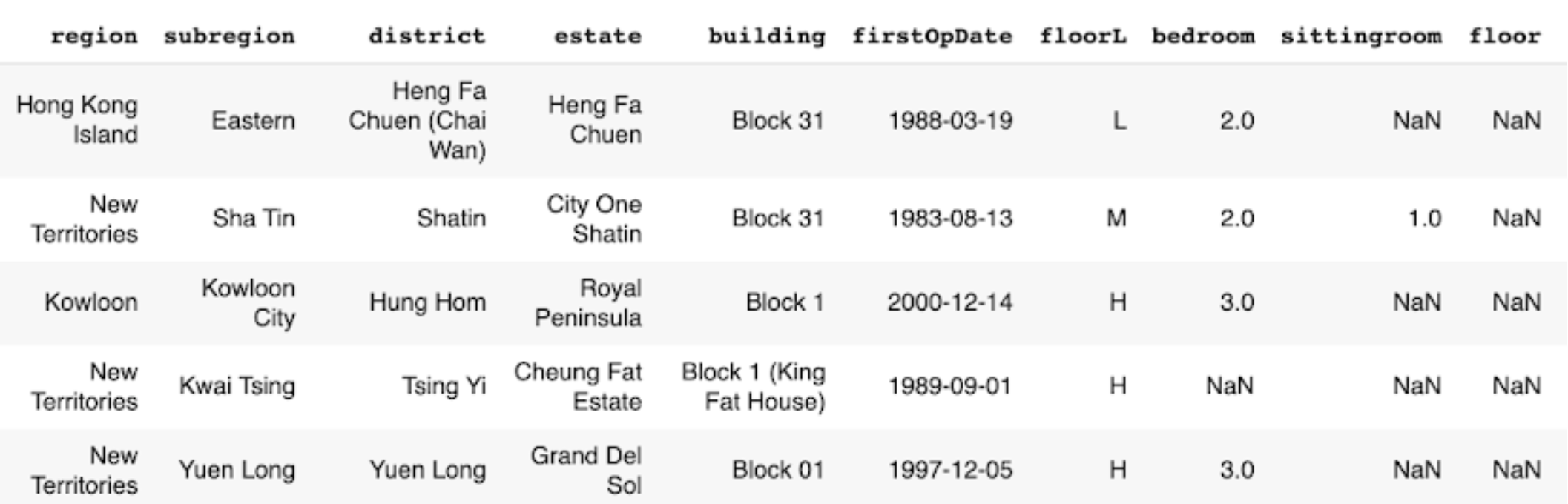

The data structure of transaction record (Midland Realty) - Part 1.¶

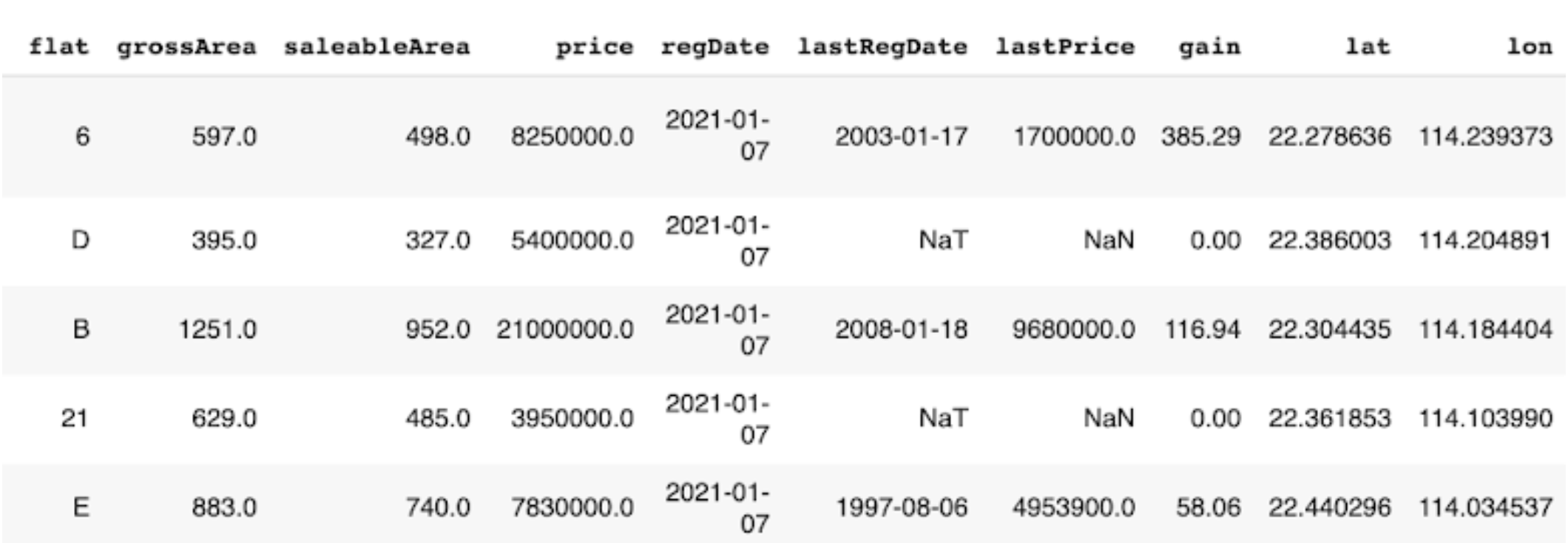

The data structure of transaction record (Midland Realty) - Part 2.¶

# Distribution

print(df['price'].describe())

# Skewness and kurtosis

print("Skewness: ", df['price'].skew())

print("Kurtosis: ", df['price'].kurt())

#output:

count 1.664090e+05

mean 9.133268e+06

std 1.310856e+07

min 5.500000e+05

25% 5.200000e+06

50% 6.830000e+06

75% 9.500000e+06

max 1.399000e+09

Name: price, dtype: float64

Skewness: 26.927207752922435

Kurtosis: 1526.4066673335874

# Calculate mean and standard deviation

data_mean, data_std = np.mean(df[feature_name]), np.std(df[feature_name])

# Calculate upper boundary

upper = data_mean + data_std * 3

# Remove outliers

df = df[df[feature_name] < upper]

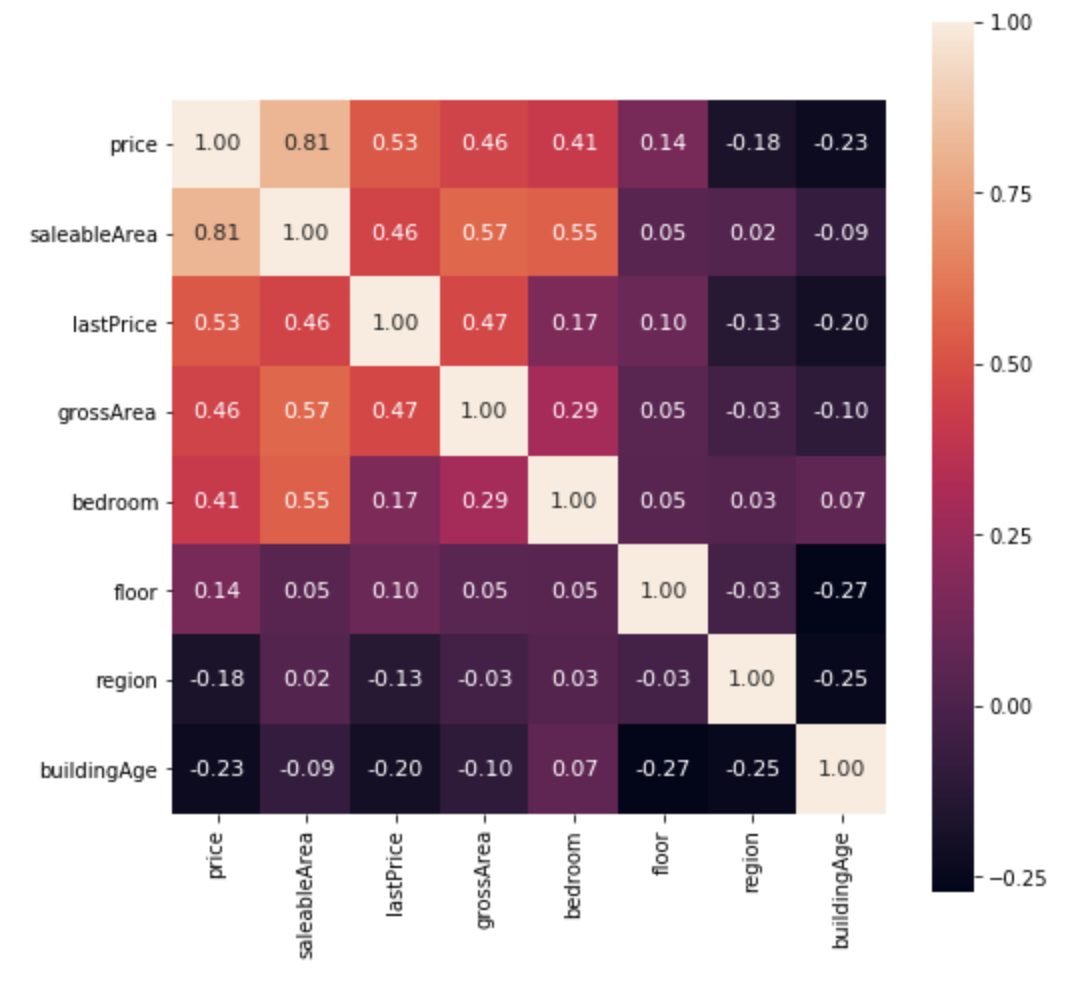

Heatmap - transaction data analysis.¶

code/macroeconomic-analysis/ in the repository.Property price prediction with machine learning¶

Train-test split¶

sklearn.model_selection.train_test_split() to split the data with the ratio

of 8:2. The input variables are the top 7 features selected from the analysis, and

the output feature is the house price.feat_col = [ c for c in df.columns if c not in ['price'] ]

x_df, y_df = df[feat_col], df['price']

x_train, x_test, y_train, y_test = train_test_split(x_df, y_df, test_size=0.2, random_state=RAND_SEED)

Log transformation¶

y_train using log function to normalise the highly

skewed price data. In this way, the dynamic range of Hong Kong’s property price can be reduced.log_y_train= np.log1p(y_train)

Training the model¶

XGBoost

Lasso

Random Forest

Linear Regression

x_train and y_train, and use the

models to make the predictions.import xgboost as xgb

# XGBoost

model_xgb = xgb.XGBRegressor(objective ='reg:squarederror',

learning_rate = 0.1, max_depth = 5, alpha = 10,

random_state=RAND_SEED, n_estimators = 1000)

model_xgb.fit(x_train, log_y_train)

xgb_train_pred = np.expm1(model_xgb.predict(x_train))

xgb_test_pred = np.expm1(model_xgb.predict(x_test))

Evaluate accuracy¶

from sklearn.metrics import mean_squared_log_error

def rmsle(y, y_pred):

return np.sqrt(mean_squared_log_error(y, y_pred))

#output:

XGBoost RMSLE(train): 0.1626671056150446

XGBoost RMSLE(test): 0.16849945199484243

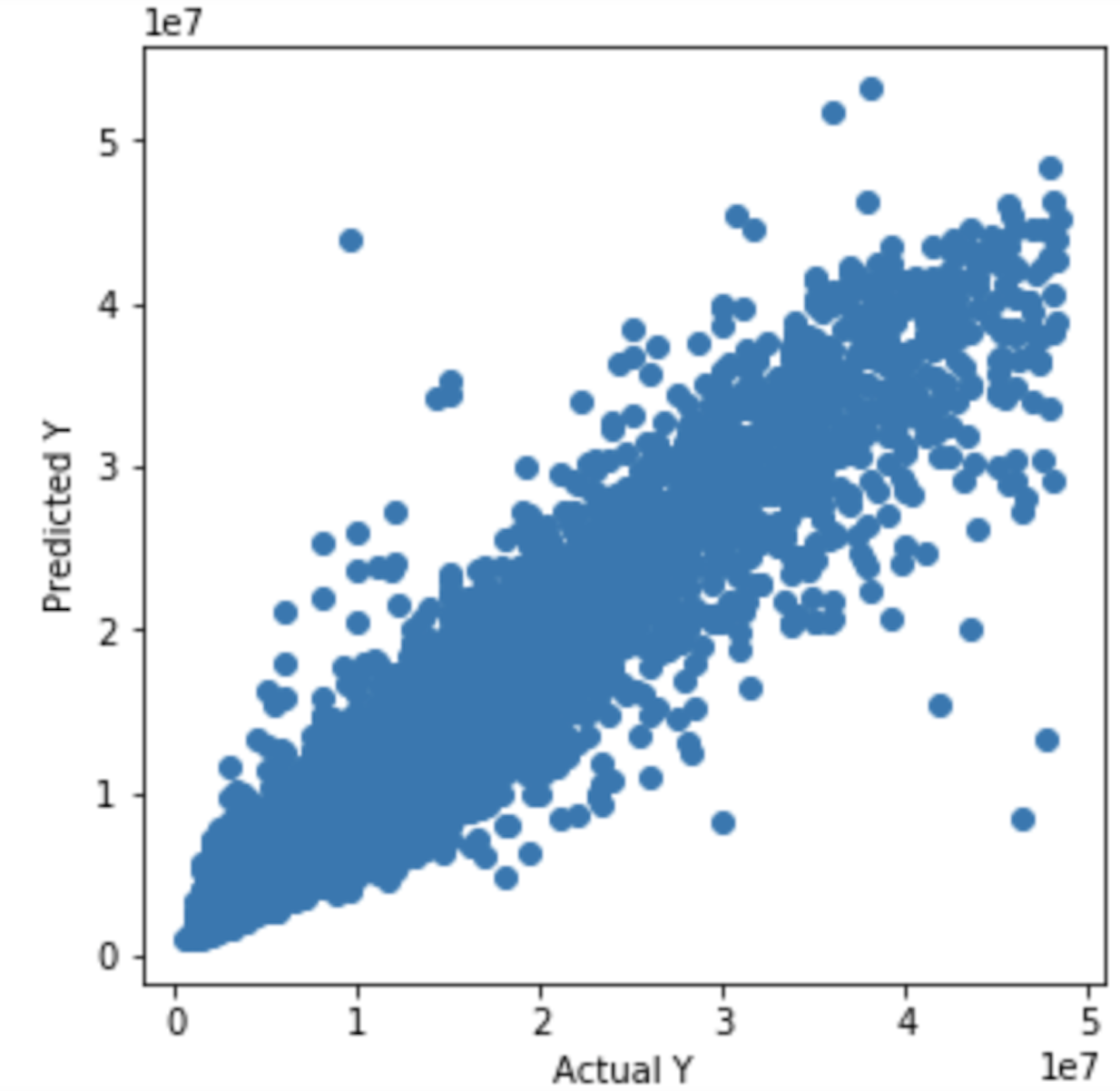

plt.figure(figsize=(5,5))

plt.scatter(y_test,xgb_test_pred)

plt.xlabel('Actual Y')

plt.ylabel('Predicted Y')

plt.show()

The graph of actual and predicted house price for XGBoost.¶

Attention