Technical analysis¶

In this tutorial, you will learn:

The basics of technical analysis

Technical analysis charts

What are the common technical indicators

How to implement technical indicators

Intro to technical analysis¶

In general, technicians consider the following types of indicators:

Price trends

Chart analysis

Volume indicators

Momentum indicators

Oscillators

Moving averages

Requirements:

Chart analysis¶

Definition

Line chart¶

plt.style.use('ggplot')

# Initialise the plot figure

fig = plt.figure()

fig.set_size_inches(18.5, 10.5)

ax1 = plt.subplot2grid((6,1), (0,0), rowspan=5, colspan=1)

ax2 = plt.subplot2grid((6,1), (5,0), rowspan=1, colspan=1, sharex=ax1)

df['50ma'] = df['Close'].rolling(window=50, min_periods=0).mean()

df.dropna(inplace=True)

ax1.plot(df.index, df['Close'])

ax1.plot(df.index, df['50ma'])

ax2.bar(df.index, df['Volume'])

plt.show()

Example of a line chart and a bar chart showing price and volume changes respectively.¶

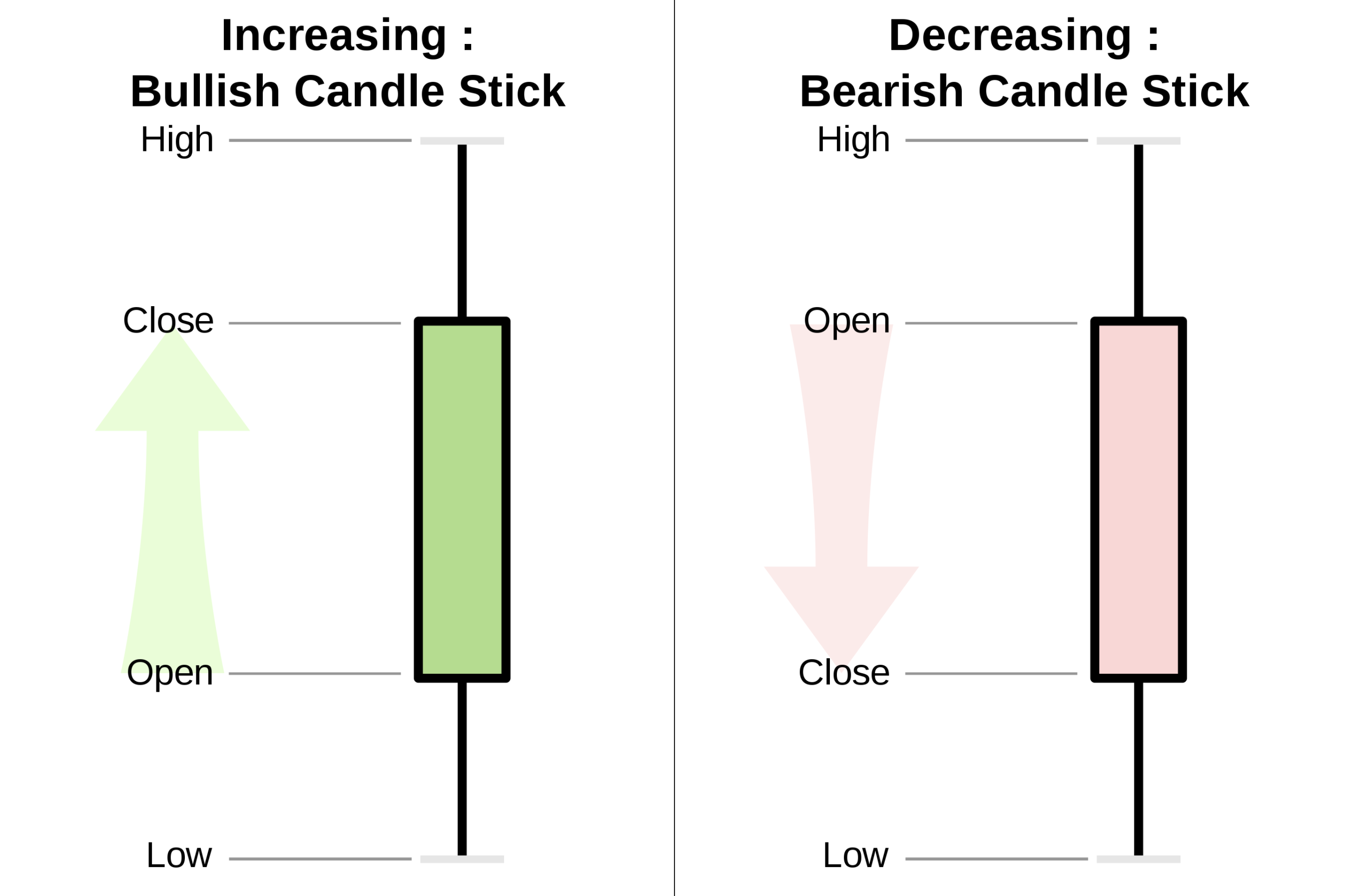

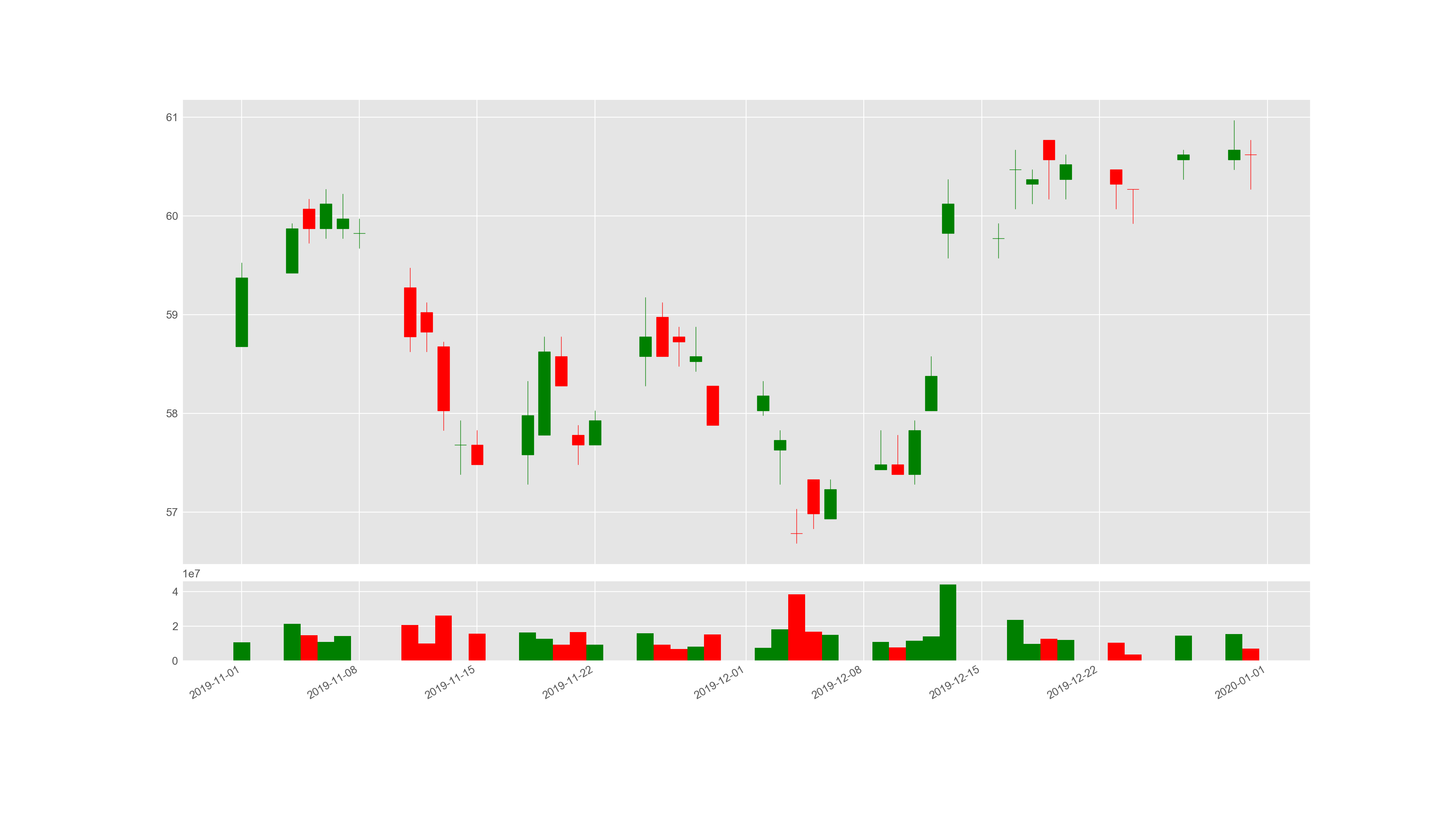

Candlesticks chart¶

mpl_finance to plot candlestick charts:fig = plt.figure()

fig.set_size_inches(18.5, 10.5)

ax1 = plt.subplot2grid((6,1), (0,0), rowspan=5, colspan=1)

ax2 = plt.subplot2grid((6,1), (5,0), rowspan=1, colspan=1, sharex=ax1)

# plot candlesticks

mpl_finance.candlestick_ohlc(ax1, data, width=0.7, colorup='g', colordown='r')

ax.grid() # show grids

############# x-axis locater settings #################

locator = mdates.AutoDateLocator() # interval automically set

ax1.xaxis.set_major_locator(locator) # as as interval in a-axis

ax1.xaxis.set_minor_locator(mdates.DayLocator())

############# x-axis locater settings #################

ax1.xaxis.set_major_formatter(mdates.AutoDateFormatter(locator)) # set x-axis label as date format

fig.autofmt_xdate() # rotate date labels on x-axis

pos = df['Open'] - df['Close'] < 0

neg = df['Open'] - df['Close'] > 0

ax2.bar(df.index[pos],df['Volume'][pos],color='green',width=1,align='center')

ax2.bar(df.index[neg],df['Volume'][neg],color='red',width=1,align='center')

plt.show()

Example of a candlestick chart.¶

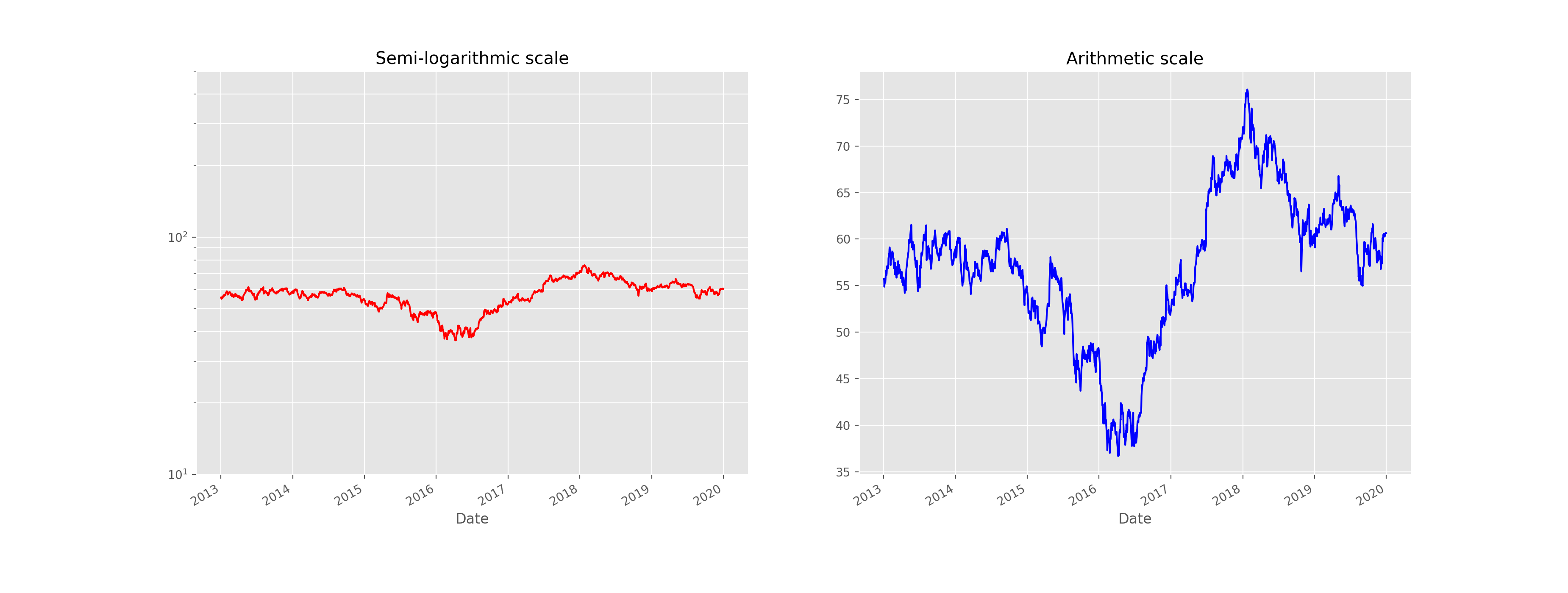

Scaling¶

Arithmetic scaling¶

Key points

On a linear scale, as the distance in the axis increases the corresponding value also increases linearly.

When the values of data fluctuate between extremely small values and very large values – the linear scale will miss out the smaller values thus conveying a wrong picture of the underlying phenomenon.

Semi-logarithmic scaling¶

Key points

On a logarithmic scale, as the distance in the axis increases the corresponding value increases exponentially.

With logarithmic scale, both smaller valued data and bigger valued data can be captured in the plot more accurately to provide a holistic view.

Therefore, semi-logarithmic charts can be of immense help especially when plotting long-term charts, or when the price points show significant volatility even in short-term charts. The underlying chart patterns will be revealed more clearly in semi-logarithmic scale charts.

plt.style.use('ggplot')

fig, (ax1, ax2) = plt.subplots(1, 2)

fig.set_size_inches(18.5, 7.0)

### Subplot 1 - Semi-logarithmic ###

plt.subplot(121)

plt.grid(True, which="both")

# Linear X axis, Logarithmic Y axis

plt.semilogy(df.index, df['Close'], 'r')

plt.ylim([10,500])

plt.xlabel("Date")

plt.title('Semi-logarithmic scale')

fig.autofmt_xdate()

### Subplot 2 - Arithmetic ###

plt.subplot(122)

plt.plot(df.index, df['Close'], 'b')

plt.xlabel("Date")

plt.title('Arithmetic scale')

fig.autofmt_xdate()

# show plot

plt.show()

The same data plotted with semi-logarithmic and arithmetic scales.¶

Technical indicators¶

code/technical-analysis_python/ in

the repository.In general, there are 2 categories of indicators:

Leading - They give trade signals when the trend is about to started, hence they use shorter periods in their calculations. Examples are MACD and RSI.

Lagging - They follow the price action, and thus gives a signal after a trend or a reversal started. Examples are Moving Averages and Bollinger Bands.

Definition

# in terminal

cd code/technical-analysis_python

python main_macd_crossover.py # run macd in the backtester

Trend indicators¶

Definition

Moving Average Convergence Divergence (MACD)¶

One of the simplest strategy established with MACD, is to identify MACD crossovers. The rules are as follows.

Tip

Buy signal: MACD rises above the signal line

Sell signal: MACD falls below the signal line

It is easy to calculate the EMA with pandas:

# Get adjusted close column

close = self.df['Close']

exp1 = close.ewm(span=12, adjust=False).mean()

exp2 = close.ewm(span=26, adjust=False).mean()

df['MACD'] = exp1 - exp2

span specifies the time span, and adjust=False means the

exponentially weighted function is calculated recursively (as we do not need

a decaying adjustment factor for beginning periods).To plot the signal line:

df['Signal line'] = self.df['MACD'].ewm(span=9, adjust=False).mean()

Moving Averages (MA)¶

We could estalish a simple trading strategy making use of two moving averages:

Tip

Buy signal: shorter-term MA crosses above the longer-term MA (golden cross)

Sell signal: shorter-term MA crosses below the longer-term MA (dead/death cross)

Here is an example of how to plotting the two MAs:

# Create short simple moving average over the short window

signals['short_mavg'] = self.df['Close'].rolling(window=short_window, min_periods=1, center=False).mean()

# Create long simple moving average over the long window

signals['long_mavg'] = self.df['Close'].rolling(window=long_window, min_periods=1, center=False).mean()

short_window and long_window on our own, for example as setting

short_window = 40 and long_window = 40.And then we could generate signals based on the two line plots:

# Generate signals

signals['signal'][short_window:] = np.where(signals['short_mavg'][short_window:]

> signals['long_mavg'][self.short_window:], 1.0, 0.0)

signals['positions'] = signals['signal'].diff()

Parabolic Stop and Reverse (Parabolic SAR)¶

(i) Rising SAR (Uptrend)

Prior SAR: The SAR value for previous period.

Extreme Point (EP): The highest high of the current uptrend.

Acceleration Factor (AF): Starting at 0.02, increases by 0.02 each time the extreme point makes a new high. AF can only reach a maximum of 0.2, no matter how long the uptrend extends.

(ii) Falling SAR (Downtrend)

Prior SAR: The SAR value for previous period.

Extreme Point (EP): The lowest low of the current downtrend.

Acceleration Factor (AF): Starting at 0.02, increases by 0.02 each time the extreme point makes a new low. AF can only reach a maximum of 0.2, no matter how long the downtrend extends.

We generate signals based on the rising and falling SARs.

Tip

Buy signal: if falling SAR goes below the price

Sell signal: if rising SAR goes above the price

array_high = list(df['High'])

array_low = list(df['Low'])

array_close = list(df['Close'])

psar = df['Close'].copy()

psarbull = [None] * len(df)

psarbear = [None] * len(df)

bull = True # flag to indicate saving value for rising SAR

af = initial_af # initialise acceleration factor

max_af = 0.2

ep = array_low[0] # extreme price

hp = array_high[0] # extreme high

lp = array_low[0] # extreme low

Then, traversing each row in the dataframe, we could calculate rising SAR and falling SAR at the same time:

for i in range(2, len(self.df)):

if bull:

# Rising SAR

psar[i] = psar[i-1] + af * (hp - psar[i-1])

else:

# Falling SAR

psar[i] = psar[i-1] + af * (lp - psar[i-1])

reverse = False

# Check reversion point

if bull:

if array_low[i] < psar[i]:

bull = False

reverse = True

psar[i] = hp

lp = array_low[i]

af = initial_af

else:

if array_high[i] > psar[i]:

bull = True

reverse = True

psar[i] = lp

hp = array_high[i]

af = initial_af

if not reverse:

if bull:

# Extreme high makes a new high

if array_high[i] > hp:

hp = array_high[i]

af = min(af + initial_af, max_af)

# Check if SAR goes abov prior two periods' lows.

# If so, use the lowest of the two for SAR.

if array_low[i-1] < psar[i]:

psar[i] = array_low[i-1]

if array_low[i-2] < psar[i]:

psar[i] = array_low[i-2]

else:

# Extreme low makes a new low

if array_low[i] < lp:

lp = array_low[i]

af = min(af + initial_af, max_af)

# Check if SAR goes below prior two periods' highs.

# If so, use the highest of the two for SAR.

if array_high[i-1] > psar[i]:

psar[i] = array_high[i-1]

if array_high[i-2] > psar[i]:

psar[i] = array_high[i-2]

# Save rising SAR

if bull:

psarbull[i] = psar[i]

# Save falling SAR

else:

psarbear[i] = psar[i]

Momentum indicators¶

Commodity Channel Index (CCI)¶

The formula for calculating CCI is given as follow.

Typical Price (TP) = (High + Low + Close) / 3

Constant = 0.015

x = Window size (default set as 20)

SMA: Simple Moving Average

signals['Typical price'] = (df['High'] + df['Low'] + df['Close']) / 3

signals['SMA'] = signals['Typical price'].rolling(

window=self.window_size, min_periods=1, center=False).mean()

signals['mean_deviation'] = signals['Typical price'].rolling(

window=20, min_periods=1, center=False).std()

signals['CCI'] = (signals['Typical price'] - signals['SMA']) /

(self.constant * signals['mean_deviation'])

A simple strategy formulated by using CCI is (the thresholds only serve as examples:

Tip

Buy signal: when CCI surges above +100

Sell signal: when CCI plunges below -100

# Generate buy signal

signals.loc[signals['CCI'] > 100, 'signal'] = 1.0

# Generate sell signal

signals.loc[signals['CCI'] < -100, 'signal'] = -1.0

Relative Strength Index (RSI)¶

where Average Gain and Average Loss are calculated as follows:

In the dataset, we need to extract gains and losses from the price column respectively:

# Get adjusted close column

close = df['Close']

# Get the difference in price from previous step

delta = close.diff()

# Get rid of the first row

delta = delta[1:]

# Make the positive gains (up) and negative gains (down) series

up, down = delta.copy(), delta.copy()

up[up < 0] = 0

down[down > 0] = 0

To calculate RS, as well as RSI:

# Calculate SMA using 'rolling' function

roll_up = up.rolling(window_size).mean()

roll_down = down.abs().rolling(window_size).mean()

# Calculate RSI based on SMA

RS = roll_up / roll_down

RSI = 100.0 - (100.0 / (1.0 + RS))

Tip

Oversold: when RSI crosses the lower threshold (e.g. 30)

Overbought: when RSI crosses the upper threshold (e.g. 70)

Rate of Change (ROC)¶

As you could see from above, it’s just the simple percentage change formula.

We could identify overbought and oversold conditions using ROC:

Tip

Oversold: when ROC crosses the lower threshold (e.g. -30)

Overbought: when ROC crosses the upper threshold (e.g. +30)

And here is one of the possible ways to calculate ROC:

n = 12 # set time period

diff = df['Close'].diff(n - 1)

# Calculate closing price n periods ago

closing = self.df['Close'].shift(n - 1)

df['ROC'] = (diff / closing) * 100

Stochastic Oscillator (STC)¶

Lowest Low = lowest low for the look-back period

Highest High = highest high for the look-back period

Note that in the formula %K is multiplied by 100 so as to move the decimal point by two places.

array_highest = [0] * length # store highest highs

for i in range(k - 1, length):

highest = array_high[i]

for j in range(i - 13, i + 1): # k-day lookback period

if array_high[j] > highest:

highest = array_high[j]

array_highest[i] = highest

array_lowest = [0] * length # store lowest lows

for i in range(k - 1, length):

lowest = array_low[i]

for j in range(i - 13, i + 1): # k-day lookback period

if array_low[j] < lowest:

lowest = array_low[j]

array_lowest[i] = lowest

# find %K line values

kvalues = [0] * length

for i in range(self.k - 1, length):

k = ((array_close[i] - array_lowest[i]) * 100) / (array_highest[i] - array_lowest[i])

kvalues[i] = k

df['%K'] = kvalues

# find %D line values

df['%D'] = df['%K'].rolling(window=3, min_periods=1, center=False).mean()

Tip

Buy signal: when %K line crosses above the %D line

Sell signal: when %K line crosses below the %D line

True Strength Index (TSI)¶

(i) Double Smoothed Price Change (PC)

PC = Current Price - Prior Price

First Smoothing = 25-period EMA of PC

Second Smoothing = 13-period EMA of 25-period EMA of PC

(ii) Double Smoothed Absolute Price Change (PC)

Absolute Price Change | PC | = Absolute Value of Current Price minus Prior Price

First Smoothing = 25-period EMA of | PC |

Second Smoothing = 13-period EMA of 25-period EMA of | PC |

Based on the above formulae, the code is shown as follow:

df['Double Smoothed PC'] = pc.ewm(span=25, adjust=False).mean().ewm(

span=13, adjust=False).mean()

df['Double Smoothed Abs PC'] = abs(pc).ewm(span=25, adjust=False).mean().ewm(

span=13, adjust=False).mean()

df['TSI'] = df['Double Smoothed PC'] / df['Double Smoothed Abs PC'] * 100

In order to interpret the TSI, we could define a signal line:

And we could observe signal line crossovers:

Tip

Buy signal: when TSI crosses above the signal line from below

Sell signal: when TSI crosses below the signal line from above

Money Flow Index (MFI)¶

It is pretty straightforward to calculate typical price:

# Typical price

tp = (df['High'] + df['Low'] + df['Close']) / 3.0

# positive = 1, negative = -1

self.df['Sign'] = np.where(tp > tp.shift(1), 1, np.where(tp < tp.shift(1), -1, 0))

# Raw money flow

df['Money flow'] = tp * df['Volume'] * df['Sign']

# Positive money flow with n periods

n_positive_mf = df['Money flow'].rolling(n).apply

(lambda x: np.sum(np.where(x >= 0.0, x, 0.0)), raw=True)

# Negative money flow with n periods

n_negative_mf = abs(df['Money flow'].rolling(self.n).apply

(lambda x: np.sum(np.where(x < 0.0, x, 0.0)), raw=True))

With the money flows, it would be easy to compute the MFI:

mf_ratio = n_positive_mf / n_negative_mf

df['MFI'] = (100 - (100 / (1 + mf_ratio)))

By way of example, we could use MFI to identify overbought and oversold conditions:

Tip

Oversold: when MFI crosses the upper threshold

Overbought: when MFI crosses the lower threshold

William %R¶

Lowest Low = lowest low for the look-back period

Highest High = highest high for the look-back period

The code for implementing %R is shown as follows:

lbp = 14 # set lookback period

hh = df['High'].rolling(lbp).max() # highest high over lookback period

ll = df['Low'].rolling(lbp).min() # lowest low over lookback period

df['%R'] = -100 * (hh - df['Close']) / (hh - ll)

Similarly, we could use %R to identify overbought and oversold conditions:

Tip

Oversold: when %R goes below -80

Overbought: when %R goes above -20

Volatility indicators¶

Bollinger Bands¶

window = 20

# Compute middle band

df['Middle band'] = self.df['Close'].rolling(window).mean()

# Compute 20-day s.d.

mstd = df['Close'].rolling(window).std(ddof=0)

# Computer upper and lower bands

df['Upper band'] = df['Middle band'] + mstd * 2

df['Lower band'] = df['Middle band'] - mstd * 2

Tip

Buy signal: when price goes below lower band

Sell signal: when price goes above upper band

Average True Range¶

1st True Range (TR) value = High - Low

1st n-day ATR = average of the daily TR values for the last n days

array_high = list(df['High'])

array_low = list(df['Low'])

tr = [None] * len(df) # initialisation

for i in range(len(df)):

tr[i] = array_high[i] - array_low[i]

atr = [None] * len(self.df) # initialisation

window = 14

atr[15] = sum(tr[0:15]) / window

for i in range(16,len(self.df)):

atr[i] = (atr[i-1] * (window-1) + tr[i]) / window

Tip

We could use ATR to filter out stocks that are highly volatile.

Standard Deviation¶

As an example, we could set window=21:

window = 21

df['SD'] = df['Close'].rolling(window).std(ddof=0)

Tip

We could use Standard Deviation to measure the expected risk of stocks.

Volume indicators¶

Chaikin Oscillator¶

df['MFM'] = ((df['Close'] - df['Low']) - df['High'] - df['Close'])

/ (df['High'] - df['Low'])

df['MFV'] = df['MFM'] * df['Volume']

df['ADL'] = df['Close'].shift(1) + df['MFV']

short_w = 3

long_w = 10

ema_long = df['ADL'].ewm(ignore_na=False, min_periods=0, com=short_w, adjust=True).mean()

ema_short = df['ADL'].ewm(ignore_na=False, min_periods=0, com=long_w, adjust=True).mean()

df['Chaikin'] = ema_short - ema_long

Tip

Buy signal: when the oscillator is positive

Sell signal: when the oscillator is negative

On-Balance Volume (OBV)¶

The formula for OBC changes according to the following 3 cases:

1) If closing price > prior close price:

2) If closing price < prior close price:

3) If closing price = prior close price then:

We could traverse the dataframe, and use if-else statements to capture the 3 conditions:

obv = [0] * len(self.df) # for storing the on-balance volume

array_close = list(df['Close'])

array_volume = list(df['Volume'])

for i in range(1, len(self.df)):

if (array_close[i] > array_close[i-1]):

obv[i] = obv[i-1] + array_volume[i]

elif (array_close[i] < array_close[i-1]):

obv[i] = obv[i-1] - array_volume[i]

else:

obv[i] = obv[i-1]

Tip

A rising OBV reflects positive volume pressure that can lead to higher prices

A falling OBV reflects negative volume pressure that can foreshadow lower prices

Volume Rate of Change¶

The way of calculating Volume ROC is similar to ROC:

n = 25 # example time period

df['Volume ROC'] = ((df['Close'] - df['Close'].shift(n)) /

df['Close'].shift(n))

Here is a simple example strategy based on Volume ROC:

Tip

Buy signal: if Volume ROC goes below zero

Sell signal: if Volume ROC is negative

References

Image sources

Attention